Žurnāls Ir | Svarīgākais politikā, ekonomikā un kultūrā

Jaunākie raksti

Policists cietumā, skolotājs – kapos. Reibuma cena Priekulē

Pēc kautiņa Priekules zaļumballē jauns policists ir nonācis cietumā, bet cienījams pedagogs — kapos. Tik traģiska ir izrādījusies divu promiļu reibuma cena

Kā 18 gadīgais Martins Bergšteins kļuva par laika ziņu seju?

Martins Bergšteins (18) vēl tikai sāks studēt ģeogrāfiju, bet viņa sacītajam jau uzticas tūkstošiem laika ziņu skatītāju Latvijā. Aiz dažām minūtēm televīzijas ēterā ir 11 gadi uzcītīga darba, mammas atbalsts un drosme turpināt meteovērojumus arī tad, kad šķiet, ka tie nevienam nav vajadzīgi

Krievija plāno viltus karoga uzbrukumus

Kulberga valdībai 70 dienas

Degvielas akcīzes samazinājums cenās nonāca daļēji

Īsi par svarīgāko ik rītu — pieraksties jaunumu vēstulei Ir Svarīgākais!

Saules aptumsumu mednieks Vitālijs Kuzmovs

Astronoms Vitālijs Kuzmovs 12. augusta Saules aptumsumu dosies vērot Maļorkā, kur tas būs pilns. Jau nākamajā dienā viņš LU Botāniskajā dārzā lasīs lekciju Perseīdu naktī. Tās apmeklētāji varēs vērot uz Zemi krītošos meteorus, vienlaikus baudot pianista Reiņa Zariņa koncertu

Kā savienot kuplu ģimeni un karjeru? Kristīne Tida to māk!

«Man ar vienu bērnu bija grūtāk nekā ir šobrīd ar pieciem. Kādai citai ir pilnīgi pretēji,» par spēju kuplu ģimeni savienot ar profesionālu izaugsmi un tikt pāri arī ļoti smagiem dzīves pārbaudījumiem saka fotogrāfe Kristīne Tīda

Pārspēti visi rekordi. Eiropas nākotne klimata pārmaiņu ugunīs

Šajā vasarā ir pārspēti temperatūras rekordi vairākās Eiropas valstīs. Plosās milzīgi mežu ugunsgrēki. Eksperti brīdina: nākotne būs vēl skarbāka

Raidieraksti

Karikatūra

Personības

«Pozitīva infekcija»

Rita Auziņa Lido sāka strādāt 18 gadu vecumā, bet jau trīs gadus vēlāk kā vadītāja atvēra restorānu lidostā. Tagad viņa ir uzņēmuma valdes priekšsēdētāja un vada to vēsturiski vērienīgākajā attīstības posmā

Ir jāsadarbojas!

Radošuma avots ir ziņkārība, bet eksportā visvairāk vajadzīga sadarbošanās, saka Andris Rubīns, kurš reklāmas nozarē strādā jau 26 gadus

No Jaunā Rīgas teātra uz pasaules malu – Matīss Ozols un viņa ceturtdaļmūža krīze

Aizgājis no Jaunā Rīgas teātra un apceļojis pasauli, aktieris Matīss Ozols (26) ir atgriezies Latvijā, lai dalītos stāstā par ceturtdaļmūža krīzi

Ne tikai dzejnieka sieva. Intas Skujenieces pēdas Latvijas ainavā

Daiļdārzniecei, dendroloģei un agronomei Intai Skujeniecei šonedēļ aprit 90 gadu. Kultūrtelpā viņu pazīstam kā dzejnieka Knuta Skujenieka sievu, bet Intai ir pašai savs stāsts un nozīmīgas pēdas, ko viņa atstājusi Latvijas ainavā

Mākslinieces Annas Faniginas runājošās rotas

Rotu māksliniece Anna Fanigina dzīvo starp dažādām pasaulēm — Latviju un Itāliju, matemātiku un mākslu, seno kultūru un šodienu. Viņa tic, ka katrai lietai dzīvē ir savs laiks

Tēlnieks Gļebs Panteļejevs: Pārticība nav brīvība

Tēlnieks Gļebs Panteļejevs (61) jaunajā izstādē un mūsu intervijā runā par monumentālām personībām, apdraudēto brīvību un vēsturi, kura nebeidzas

Viedokļi

Satura mārketings

: Māris Gaugers, Ansis Valdovskis, Toms Lācis, Rolands Levics, Matīss Zemītis")

Bizness un ekonomika

dibinātāja.")

No vakances līdz komandai

Danas Kocānes personāla atlases uzņēmums Teamence savieno īstos uzņēmumus ar īstajiem cilvēkiem

Spēks ir detaļās

Pēc 18 gadiem ēdināšanas biznesā Vīnkalnu picēriju dibinātājs Artis Žentiņš kopā ar dizaineru Aigaru Lauzi radījis jauna tipa profesionālas picu krāsns prototipu. Tagad Dimantiņš jāpārvērš ražojamā un eksportējamā produktā

Pētījumi

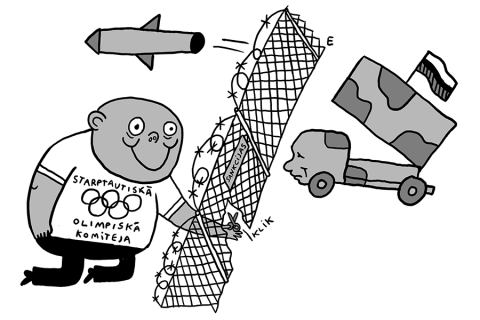

Noslēpumaina raķešu rūpnīca Latvijā. Kas stāv aiz vērienīgā priekšvēlēšanu solījuma?

Ekonomikas ministra parakstīts memorands sola Latvijā būvēt artilērijas raķešu rūpnīcu, taču ASV investoram nav artilērijas ražošanas pieredzes, un arī mūsu bruņotie spēki šādas spējas neplāno

Nevajag baidīties!

Produktivitātes rādītājs Latvijā ir krietni zem Eiropas Savienības vidējā. To var palīdzēt kāpināt mākslīgā intelekta rīku izmantošana. Taču — kā tā mainīs dažādas profesijas un tajās nepieciešamās prasmes?

Pamatskolas eksāmenos izkrīt katrs 20. devītklasnieks. Ko darīt?

Vairāk nekā 800 jauniešu šogad nepabeidza pamatskolu, jo nespēja pārvarēt eksāmena nokārtošanai nepieciešamo 15% slieksni. Tas ir vidēji katrs 20. devītklasnieks jeb viens no klases. Iemesli meklējami ne tikai skolā, bet arī ģimenē

Pieci gadi pēc novadu reformas. Vai kritiķi mainījuši viedokli?

Kāpēc piecus gadus pēc novadu reformas kādas Latvijas pašvaldības vadītājam ir kauns iet pa ielu, bet cits atzīst — beidzot redz gaismu tuneļa galā?

un vidusskolai (10. klasei). Foto — Marta Āboltiņa")

Kāpēc Pierīgā trūkst vietu 10. klasēs un kādi ir risinājumi?

Iedzīvotāju skaita pieaugums Pierīgā un jauniešu vēlme mācīties labākajās vidusskolās izveidojusi milzu drūzmēšanos pie 10. klašu durvīm. Ko darīt, lai vidusskolā neuzņemtie nejustos lieki?

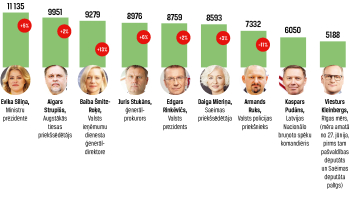

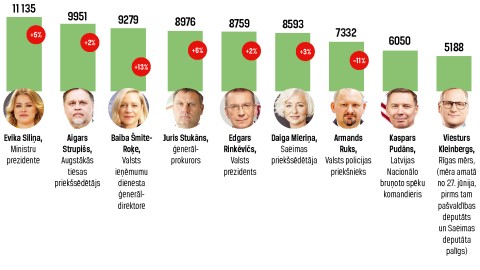

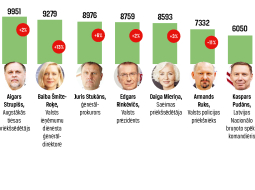

Kuras valsts amatpersonas pelna visvairāk?

Kuras valsts amatpersonas 2025. gadā visvairāk nopelnījušas, un kuras iekūlušās lielākajos parādos

Ams, ams, ams! Vai dzejoļi apdraud bērnus?

Ivara Šteinberga dzejas krājums sociālajos tīklos izraisījis asas diskusijas par tabu tematiem bērnu literatūrā. «Kopā ar grāmatu aicināja dedzināt arī mani pašu, draudēja tādus kā mani arī nošaut,» saka dzejnieks

Vecrīgas pulksteņu laupītāju kļūdas, kas noveda viņus aiz restēm

Vecrīgas luksusa pulksteņu veikala trīs aplaupītāji atzinuši vainu un saņems cietumsodu, bet ceturtais uzbrucējs joprojām ir brīvībā. Izmeklētāji atklāj, kādas trīs kļūdas palīdzēja tikt šiem noziedzniekiem uz pēdām

Eiropā

VIDEO: Vai Eiropai ir vajadzīga Turcija?

Neraugoties uz autoritārisma tendencēm, Turcija ir ES stratēģiskais partneris.

VIDEO: Vai Eiropai joprojām nepieciešami skaidras naudas norēķini?

Eiropa pēc gadiem ilgas virzības uz bezskaidras naudas norēķiniem sāk apzināties šīs pieejas riskus.

VIDEO: Kā risināt Eiropas nepilngadīgo noziedzības problēmu?

Pieaugot jauniešu noziedzībai, dažas ES valstis vēlas pazemināt kriminālatbildības vecumu.

VIDEO: Vai Eiropa spēj stāties pretī dronu apdraudējumam?

Kopš kara sākuma Ukrainā Eiropā arvien biežāk ielido militārie droni, tāpēc ES plāno veidot pretdronu vairogu.

VIDEO: Vai futbols piedzīvo identitātes krīzi?

Aiz Pasaules kausa spožās fasādes slēpjas futbola pasaules tumšā puse

VIDEO: Migrantu atgriešanas centri — risinājums vai pārspīlējums?

Lai paātrinātu izraidīšanu, ES plāno atļaut veidot migrantu atgriešanas centrus ārpus savām robežām.

VIDEO: Kā cīnīties ar viltus speciālistiem estētiskās medicīnas nozarē?

Nelegālas botoksa klīnikas un injekcijas bez speciālista uzraudzības apdraud cilvēku veselību.

VIDEO: Cik korumpēta ir Eiropa?

Spānijā un Francijā politiķi stājas tiesas priekšā saistībā ar kukuļošanas skandāliem.

Recenzijas

O, vēder! Nekrologs jūrasgovij

Romāns Ardievu, teiksmainie! ir vienas sugas iznīcības traģiskais stāsts

Grāmata, kuru nesapratu

Ingas Gailes stāsti krājumā Ievērojamu cilvēku dzīve ir kā caurspīdīgas kolbas

Simt gadi Ungārijā

Jaunais šveiciešu rakstnieks ar romānu Lāzāri kļuvis par Eiropas literatūras brīnumbērnu

Populārākie raksti

Kaucmindes pils atjaunotāja bez rozā brillēm

Pēc 30 gadus ilguša sabrukuma un neskaitāmu īpašnieku maiņas unikālās Kaucmindes pils logos beidzot iespīdējis cerību stars, jo jaunie īpašnieki apņēmušies to patiešām atjaunot

Kuras valsts amatpersonas pelna visvairāk?

Kuras valsts amatpersonas 2025. gadā visvairāk nopelnījušas, un kuras iekūlušās lielākajos parādos

Vecrīgas pulksteņu laupītāju kļūdas, kas noveda viņus aiz restēm

Vecrīgas luksusa pulksteņu veikala trīs aplaupītāji atzinuši vainu un saņems cietumsodu, bet ceturtais uzbrucējs joprojām ir brīvībā. Izmeklētāji atklāj, kādas trīs kļūdas palīdzēja tikt šiem noziedzniekiem uz pēdām

Konrāda kvartāls Cēsīs – jaunais iemīl veco

Māju pa mājai arhitektūras mantojuma atjaunotāju kopienai pievienojies tehnoloģiju zīmola Draugiem Group uzņēmums Mājas Cēsīs. Vasaras pilnbriedā sabiedrībai atvērts Konrāda kvartāls — vecās un jaunās arhitektūras ansamblis Cēsu vecpilsētā

No Jaunā Rīgas teātra uz pasaules malu – Matīss Ozols un viņa ceturtdaļmūža krīze

Aizgājis no Jaunā Rīgas teātra un apceļojis pasauli, aktieris Matīss Ozols (26) ir atgriezies Latvijā, lai dalītos stāstā par ceturtdaļmūža krīzi

Policists cietumā, skolotājs – kapos. Reibuma cena Priekulē

Pēc kautiņa Priekules zaļumballē jauns policists ir nonācis cietumā, bet cienījams pedagogs — kapos. Tik traģiska ir izrādījusies divu promiļu reibuma cena

Ams, ams, ams! Vai dzejoļi apdraud bērnus?

Ivara Šteinberga dzejas krājums sociālajos tīklos izraisījis asas diskusijas par tabu tematiem bērnu literatūrā. «Kopā ar grāmatu aicināja dedzināt arī mani pašu, draudēja tādus kā mani arī nošaut,» saka dzejnieks